The Government’s New auto-enrolment pension scheme was approved earlier this morning and is set to come into effect in early 2024 for approximately 750,000 workers across the State.

The scheme has been in the works for several years and was initially planned to come into effect this year but was delayed due to the Covid-19 pandemic.

The scheme itself is being brought because of the pensions time bomb coming down the line due to not enough people having an occupational or supplementary pension for when they retire.

Who is impacted by the auto-enrolment scheme?

The Government confirmed this morning that there are approximately 750,000 people between 23 and 60 who are employed and not currently enrolled in an occupational pension scheme.

These 750,000 people are being targeted through the auto-enrolment scheme to ensure that they begin saving for their pension and that they are not left on just the State pension when they retire.

How does the scheme work?

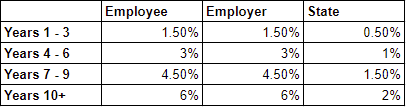

The new plan will see contributions paid by employees being matched by their employers as a percentage of the employee’s gross income.

The State will also add a top-up to the money paid into the pension pot.

For example, an employee could pay in €3 to their pension. This means that employers must match that €3 and the State will top it up by €1.

The contribution rates are set to be phased in over a decade as follows:

As the scheme is opt-out rather than opt-in, people without an occupational or supplementary pension will not need to do anything to start paying into their pension fund.

Can I opt-out of the scheme?

Yes, employees who do not want to pay into the scheme are able to opt out, but this cannot be done immediately.

According to Social Protection Minister Heather Humphreys, anyone who is accessing the scheme will have to wait six months after it starts until they are able to opt-out.

After this, any money that they have saved in that six months may be returned to them, but contributions paid by both employers and the State will remain in the pension pot.

However, this is not an indefinite opt-out and employees will be automatically opted-in after two years.

The same procedure applies, where they will have to wait six months before they can opt back out again.

Are contributions capped?

Both employer and State contributions are capped at a maximum of €80,000 of an employee’s gross annual salary.

However, employees can contribute on earnings greater than €80,000 if they wish.

I have a Personal Retirement Savings Account (PRSA). Can I sign up for the new scheme when it is rolled out?

At present, elements of this are still being worked out.

When asked by The Journal about this issue, Humphreys said that under current plans people can have a paid up PRSA pot and then join the new auto-enrollment scheme while leaving the PRSA pot where it is.

Humphreys then added that the Department is checking to see whether or not it is possible to have the PRSA in operation alongside the new auto-enrollment scheme.

“There’s there’s a bit of detail to be worked out on that but we’re trying to make it as attractive as we can because people who did, in fairness, sign up to the PRSA, we want to make sure that they’re looked after as well because they’re not getting the employer contribution.”

According to Tim Duggan, assistant Secretary General at the Department of Social Protection, the first priority is the 750,000 people who do not have any pension provision and when they are looked after, legal matters around PRSA pension pots will be tackled.

“The focus initially is on the 750,000 people who don’t have any provision and then subsequent to that, we’ll be trying to see how we can make the system facilitate people who already have arrangements but would prefer to switch.”

Can I drawdown my pension early under the new plan?

In most circumstances, no, people will not be able to drawdown their pension early through the new scheme.

Currently the only circumstance where someone can drawdown their pension through this proposed scheme before their retirement age is an extreme illness.

“There won’t be earlier drawdown than the retirement age for any other circumstances,” said Duggan.

According to Duggan, the specifics of pension drawdown through illness will be worked on when the legislation is drafted later this year.

In 2024, when the new scheme is set to be in place, the pension age will still be 66.

Can I contribute lump sums to the new pension scheme?

Currently, no. Humphreys said that the immediate plan is to get the scheme up and running before they look at allowing additional voluntary contributions.

However, Humphreys said it is something that they can examine after the scheme is up and running.

Where are my savings going?

Employees who are enrolled in the new scheme will have four different retirement savings funds to choose from.

These funds will all have different risk/reward profiles, going from conservative, medium-risk to high-risk. There will also be one default fund based on what the Department calls a ‘life-cycle’ investment profile.

Anyone who does not choose a specific fund will be enrolled in the default fund.

Will the State pension remain in place?

Yes, Humphreys confirmed that the State pension will remain and will be the “bedrock” of the new auto-enrolment scheme.

Source: The Journal, 29/03/2022

How we help

We can help take the effort out of this for you by demonstrating how this would work for you and your family and providing you with one cohesive Financial Plan.

You can arrange a meeting by clicking here to access my diary, email info@smartfinance.ie or alternatively, call me on 087 8144 104.